Arc of the Covenant: Dispatches From Seoul Advocate for Documentation Discipline

April 16, 2026

I was delighted to attend the PDI Seoul Forum this week. Two hundred and fifty attendees, fourteen countries, and a program built around the question every allocator in the room was already asking. What is behind the recent private credit headlines, and should it change how capital gets deployed from here?

The headlines had done the work of setting the mood. Recent high-profile defaults at names that had been passed around the lending market for years. A blown merger and redemption queues at one of the largest open-ended vehicles. BDC trade-downs after the US rate cuts. Morgan Stanley forecasting 8% defaults. The chair of a major US bank telling the market that where there is one cockroach, there are more.

Inside the room, the tone was more measured. Every panel reached the same conclusion within the first ten minutes: these are retail-structure and manager-selection problems, not asset-class problems.

One European manager cited two decades of internal loss data showing their junior credit losses running at roughly a ninth of market rates. Another panelist pointed out that the ten largest global managers have 30 to 40% portfolio overlap with each other, which makes allocating across them a concentration trade dressed as diversification. On the cockroach point, one GP noted dryly that one of the deals in question was originated by the very bank now warning about infestations.

The diagnosis was widely shared. The fixes all circled back to documentation.

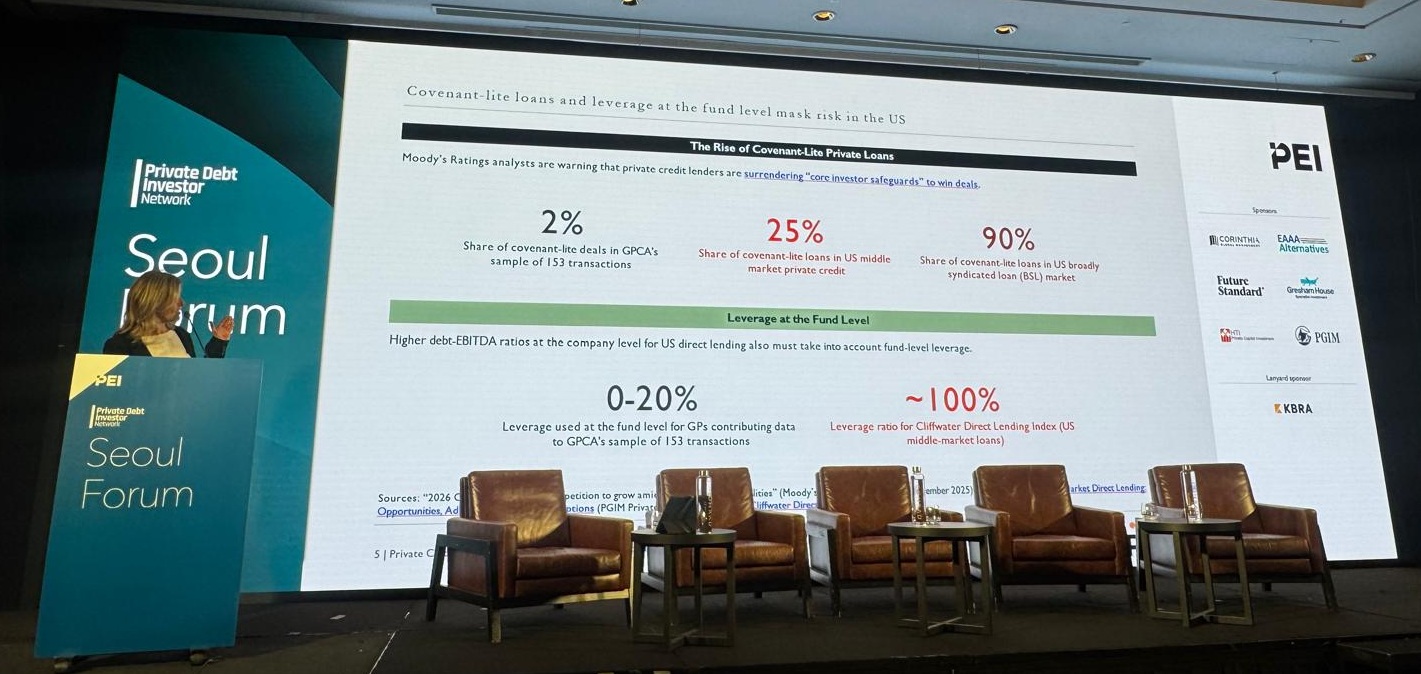

Some compelling numbers from CEO Cate Ambrose’s presentation of the Global Private Capital Association report “Private Capital Outlook: Assessing Opportunities Beyond the U.S.” (in the blog image):

- Cov-lite share outside the US and Western Europe runs at 2% of transactions. In US mid-market it is 25%, and in the US broadly syndicated loan market it is 90%.

- Fund-level leverage 0 to 20% in the same non-Western sample, against roughly 100% on the Cliffwater Direct Lending Index for US middle-market loans.

A US manager warned that recoveries on cov-lite large-cap deals will disappoint when the cycle turns. Another panelist made the point that EBITDA definitions permitting 30% pro-forma run-rate add-backs render covenant cushions largely decorative. The work, then, is in the drafting. Covenant cushions, EBITDA definitions, fund-level leverage, and side letter terms carry the real risk.

The Asian LP angle matters here. A government strategy academic previewed a more risk-tolerant Korean policy environment, including direct capital-market routes and tax-deferral structures tied to growth-fund investment. A senior allocator described a deliberate tilt toward European mid-market and secondaries, citing structural features rather than yield-chasing. A European fund-of-funds shared that its private credit book runs roughly 30% Europe and 70% US, with a migration toward lower mid-market where spreads still compensate for the work involved. Korean LPs are asking sharper questions about FX hedging, side letters, and EBITDA definitions than the market gives them credit for.

Three takeaways for credit documentation specialists:

- The default conversation has moved past “will defaults rise” to “what will recoveries look like.” That is a covenant question.

- Cross-manager portfolio overlap at the top of the market means single-deal documentation analysis can understate portfolio-level risk. LPs holding multiple large funds may be underwriting the same borrowers several times over.

- AI disruption risk in software credits is a maturity-wall and covenant-cushion question. Most at-risk names can adapt, but they will refinance on terms that matter to lenders.

The consensus in Seoul was that the next twelve months will reward managers who can read documents and penalize those who cannot. That is the conversation Arc of the Covenant was built for.